When You Should Use a Real Time Inventory System

Pros and Cons of Real Time Inventory

Real time inventory systems offer many clear, easily understood advantages in terms of actively managing and optimizing inventory levels. A well-managed real time inventory system allows you to see exactly where stock is, the levels it’s at, what is on back order, what is allocated to existing sales, what needs reordering and when. All great tools for physically managing inventory effectively. However, there is another advantage to a real time inventory system that is equally useful, but frequently misunderstood.

How a Real Time Inventory System interfaces with your business accounts. And why it’s a good thing!

One of the primary concepts of good accounting, and one of the most difficult to implement, is allocating the Cost of Goods Sold accurately against the Income associated with those goods. The lapse of time between goods being manufactured or purchased and the final product being sold mean the simple flows of money in and out of accounts over time does not accurately measure Net Profit over time.

See the example below.

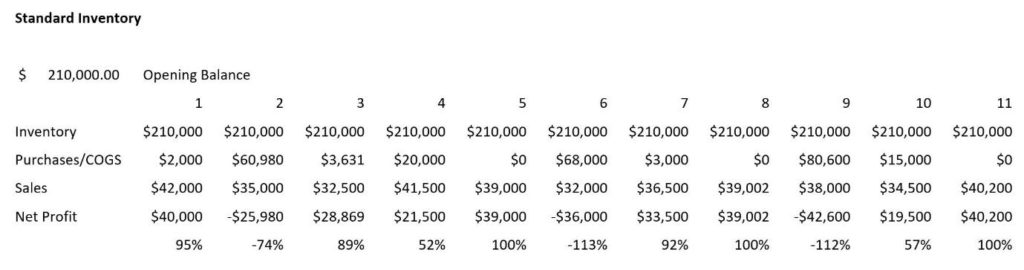

Standard Account System – No real time Inventory

- Purchases are coded directly as Cost of Good Sold – even though these coded costs might not relate to the items being sold in that same period.

- Net profit is calculated Sales Less Purchases (COGS) for a determined period. (often a month, 3 months or a year)

- The only time the stock level is adjusted is when a stock take is done, usually at the end of the financial year. At that time a stock adjustment entry is done, usually by your accountant for tax accounts.

- If the inventory value has decreased from one Stocktake to another the Stock Value is adjusted down and the Cost of Good Sold is adjusted up. Because the costs show higher, the net profit will move down.

- If the inventory value has increased the Stock Value is adjusted up and the Cost of Good Sold is adjusted down, the net profit will move up.

As you can see on the example below the Net Profit as a percentage of sales can bounce around quite bit over the year. You do not have an accurate Net Profit figure until the stock adjustment at the end of the financial year.

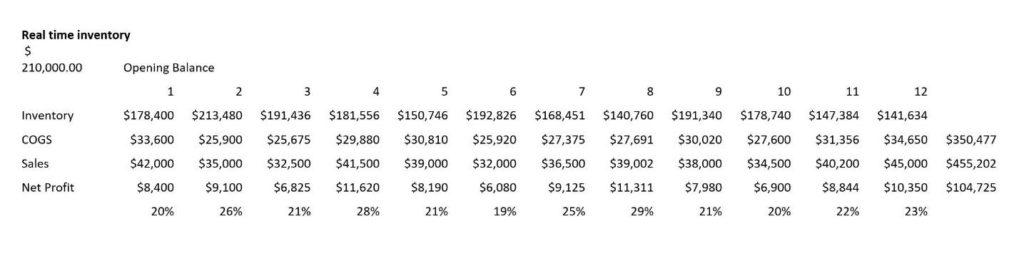

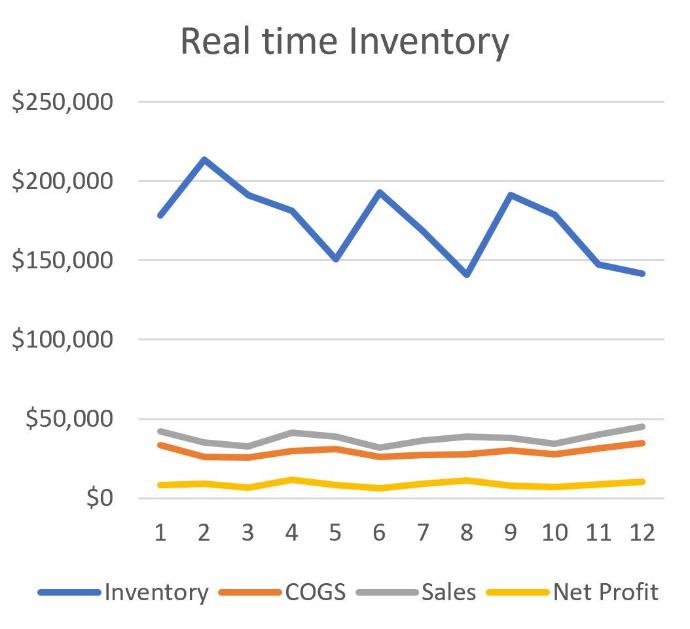

Account System - With real time Inventory

Purchases are coded as Inventory, increasing the inventory asset when stock comes in.

When the stock is actually sold, the costs are allocated to Cost of Goods Sold – and not before. So at the time of the sale, Cost of Goods Sold is increased and the Stock asset value decreased.

Because the COGS is interfaced at the point of sale the Stock value in the account should always match the real time value of stock, and the Net Profit, Sales Less COGS should be accurate over time. See example below:

Living Business will find creative ways to help you and can configure the inventory management solution best suited to your company’s needs. Get in touch with us to find out more.